Eliminate Buddy Punching by Adding Biometrics To Your Time Clock

How would you like to save 5% per year on your employee labor costs by doing one simple thing? The American Payroll Association estimates that “buddy punching” accounts for up to 5% of gross payroll costs each year. For a company with a yearly labor cost of $300,000, buddy punching could cost as much as $15,000.

How would you like to save 5% per year on your employee labor costs by doing one simple thing? The American Payroll Association estimates that “buddy punching” accounts for up to 5% of gross payroll costs each year. For a company with a yearly labor cost of $300,000, buddy punching could cost as much as $15,000.

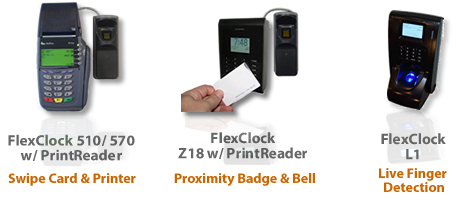

Our New PrintReader™ Can Add Biometrics To Your Existing System

Eliminate buddy punching by adding biometrics to your already-existing time clock with our NEW PrintReader™! Now a biometric solution can be easily added to your existing timekeeping system in just a few minutes. Saving on labor costs and preventing employee time theft by eliminating buddy punching will save your company thousands in labor costs each year while improving employee productivity.

Start Your Free 30-Day Timekeeping Trail Today

Not sure if a timekeeping system is right for you? Call Vision Payroll today to get started on your free 30-day timekeeping trial. A few clicks on the internet, import your employees, and you’re ready to go. Find out how a modern, automated timekeeping system can save time and money, improve your recordkeeping, make the entire payroll process much simpler.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Vision Payroll